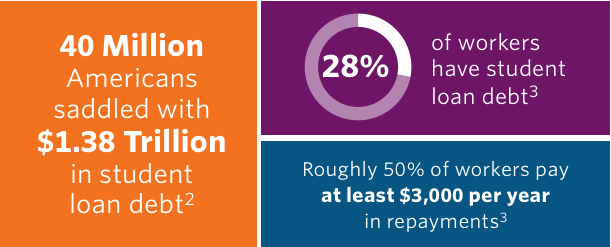

Student debt is a hot topic among benefits leaders for many reasons. It’s a huge source of stress for employees of all ages as multiple generations use loans to help themselves, or family members, pay for college. Plus, a whopping 70% of college students rely on loans—nearly $40,000 on average—to pay for school.1

This issue has been top of mind for retirement plan administrators who’ve worried about how student debt is impacting employees’ financial well-being as well as their ability to save enough for retirement.

According to a recent study by Fidelity, big sources of stress for most employees are work and finances. Of the 9,000 employees participating in the survey, saving for the future (34%) and paying off debt (33%) caused high levels of stress.4

Stress over debt is linked to lower productivity as well. The study also found that employees with the highest levels of debt have twice the absenteeism rates of those with the lowest debt levels.4

But there’s good news on the horizon: New guidance from the IRS could help employees prioritize both retirement saving and student-debt repayment. A recent IRS ruling (PDF) approved a company's pretax contributions to an employee’s 401(k) account if the employee is making student-loan repayments of at least 2% of their salary for a given pay period.5 This would allow employees to build retirement savings through employer contributions—even if they’re not making individual contributions.

The private-letter ruling doesn't apply to other companies. However, it sets a precedent for what's possible in addressing student loan debt within the 401(k) realm.

This is great news, especially for young workers who, by not participating in the 401(k), could miss out on the crucial years they need to build retirement savings. It may also help employers, looking to attract young, educated workers, better align their benefits offerings with employee needs.

We’re very excited about this ruling, because it has the potential to address a huge need. Helping employees improve their financial well-being is no easy task, and this is a great step forward. It’s especially compelling because of the meaningful impact it could have on those critical early years of saving—when the power of compounding can help account balances grow dramatically. And like the magic of compounding, the impact of this change could profoundly improve the retirement readiness of future generations of Americans.

For tips on how to help your employees improve their financial well-being, read our guide, 6 Steps to Bring Financial Wellness to the Workplace, and watch our webinar, Rethinking Well-being: Integrating Health and Wealth.

We're proud to work with large employers who recognize the business value of engaging employees in benefits. If you want to learn more, contact us.

1 “Here’s how much the average student loan borrower owes when they graduate,” CNBC, February 15, 2018.

2 “Quarterly Report on Household Debt and Credit,” Federal Reserve Board of New York, February 2018.

4 Total Well-being Survey, Fidelity, August 2018.

5 “IRS clears way for student loan benefit tied to 401(k),” ebn, August 20, 2018.